In this extract from UK Housing Review, Peter Williams says rising pressures from supply shortages, higher interest rates, Covid, war in Ukraine and more have become familiar – and the housing market is no exception.

In this extract from UK Housing Review, Peter Williams says rising pressures from supply shortages, higher interest rates, Covid, war in Ukraine and more have become familiar – and the housing market is no exception.

After two years of buoyant activity, propelled in part by governments across the UK cutting transaction taxes, the prospects for both owners and renters are worsening.

Many first-time buyers and others brought forward their purchases to take advantage of tax cuts. Further momentum came from buyers moving quickly to seal longer-term mortgage deals ahead of rate rises. The upsurge in demand along with locational effects and the ‘race for space’ kept prices rising, despite the pandemic. Sellers upped prices and bidding wars broke out, driving prices even higher.

Some of these dynamics remain but are waning alongside the emerging financial squeeze. Some 40% of mortgage products have been withdrawn from the market, partly because of the volatility of the swap market on which fixed-term mortgages are based. There’s also been a general re-pricing of products to reflect the rise in base rates and gilt yields.

Clearly all data now lag behind market realities as sellers begin to chase buyers: the tables have turned. Price rises appear to be slowing but we await evidence of the almost inevitable market contraction and falling prices – but much depends on buyer segment, property location and type, and, of course, on government and Bank of England interventions. Sales at the bottom end of the market may fall more rapidly reflecting the surging pressures on lower-income households. Recently announced transaction-duty cuts will stimulate demand – but how far will they offset the negative factors?

Completion prices reflect the market three months ago so are a lagged indicator. The RICS Residential Market Survey for August showed that enquiries, sales and instructions were falling ever faster. Prices were still rising but more slowly, suggesting an imminent halt. Somewhat dated figures show that numbers of approved mortgages and transactions have been falling over the last few months – but, of course, with a shortage of homes on the market, prices have stayed strong.

Without doubt the market (as measured by house prices) has proved to be more resilient than many expected, in part due to limited stock being available and enhanced demand. With sharp interest-rate rises now coming through in mortgage pricing and with confidence plummeting, this will change. Some 80% of borrowers are on two- and five-year fixed rates but when these end, loans will be more expensive. House-price indices are starting to point towards monthly nominal price falls.

The trends are reflected in the Treasury’s Comparison of Independent Forecasts. Forecasts for Q4, 2022 range from +12% rise in house prices to +0.8%. The median is +6.2%, whilst OBR had projected +4.3%. Projections for 2023 reveal a narrower, more negative range from +3.5% down to -4.8%. This suggests a significant slowing in the market and real-terms falls in prices. Although mortgage arrears and possessions remain low, the new conditions suggest that more households will get into difficulty.

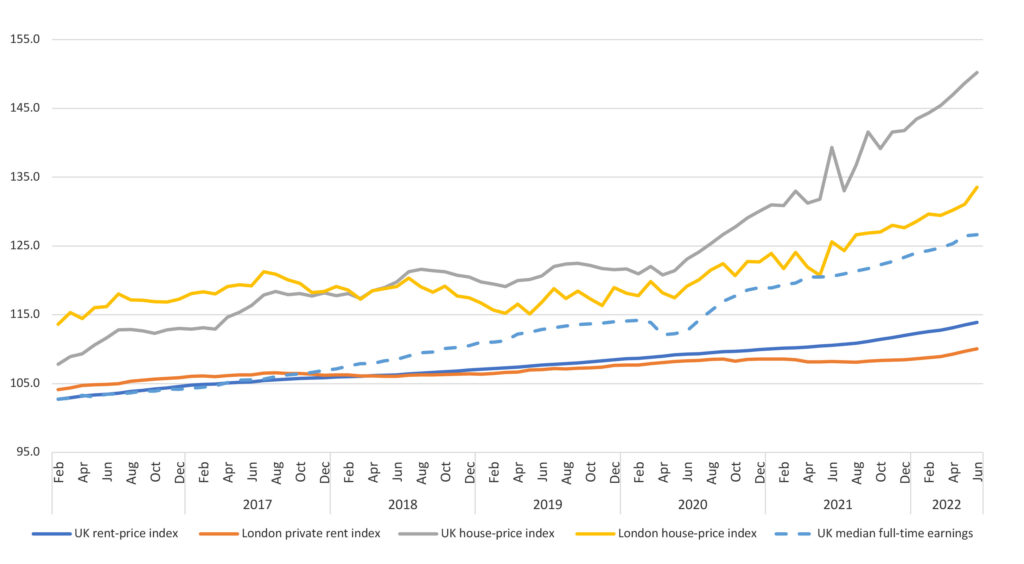

Stretched affordability is no longer just a feature of London and the South East. Setting aside rising mortgage costs and possibly falling prices, the cost of renting has surged, reducing the capacity of some households to save a deposit. Demand in the PRS has increased in part due to people returning to the cities and from parental homes, while supply has fallen. Evidence suggests that the PRS is now shrinking, partly in response to the policy stance of governments across the UK.

The tightening regulation of the PRS is likely to be accompanied by fewer affordable homeownership opportunities, with the planned closure of the English Help to Buy scheme in March 2023 and less provision of shared ownership by housing associations as they respond to pressures on their finances.

The Financial Policy Committee’s decision to end the interest-rate stress test (which assesses a borrowers’ ability to repay a mortgage) offers some slight mitigation. The FPC’s technical annex suggests 6% of borrowers may have borrowed more without the limit and that around 1% of renters might have been prevented from buying.

Whereas in 1991 about two-thirds of 25–34-year-olds were homeowners, it’s now around two-fifths. Affordability pressures on younger households have increased and the inequalities driven by the housing market, for both owners and renters, are intensifying. While regional levelling-up may help, it’s the UK government’s fiscal policy and its willingness to make some hard choices around property taxation that need most attention. There’s no sign of that.